Davidson Investment Advisors’ third-quarter commentary provides insights into the U.S. equity, taxable fixed income, municipal fixed income, and international equities markets.

International Equities Market

Trade Agreements Drive Risk-On

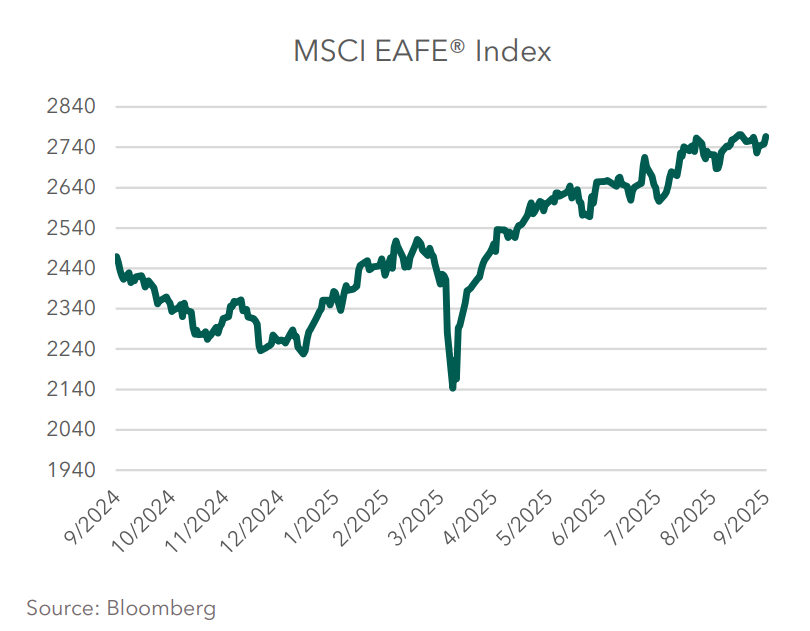

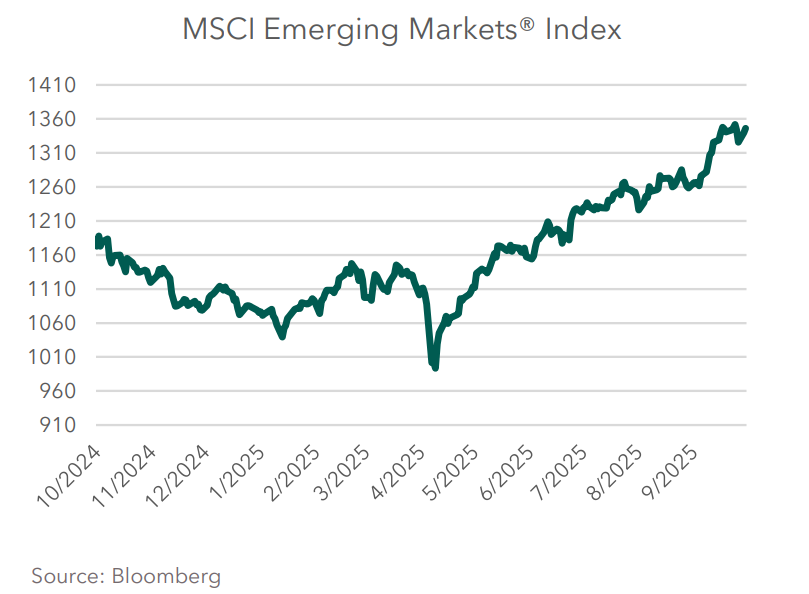

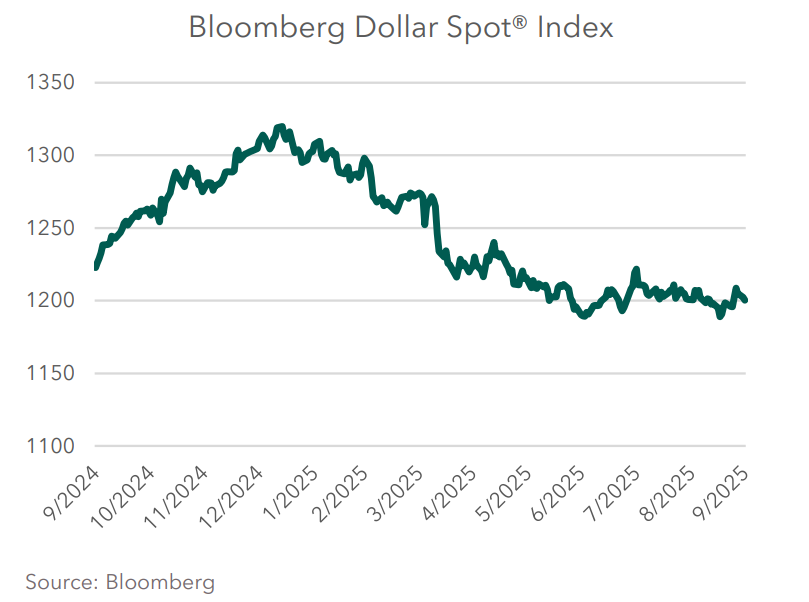

Equity performance was strong across markets during the third quarter. The MSCI Emerging Markets® Index performed best, returning 10.6% for the quarter. Domestic equities, represented by the Russell 3000® Index, returned 8.2% for the quarter whereas the MSCI EAFE® Index, our proxy for developed international equities, generated a return of 4.8%. International equities continue to outperform domestic equities on a year-to-date basis with the Emerging Markets Index up 27.5% and the MSCI EAFE Index up 25.1% versus the Russell 3000® Index up 14.4%. The dollar strengthened modestly, with the Bloomberg U.S. Dollar Spot Index up 86 basis points and was a moderate headwind to international equity performance.

The tariff picture is slowly beginning to come into focus with a number of preliminary agreements announced during the quarter. One thing that is very clear is the Trump Administration is set on changing global trade. Several country representatives remarked that once they accepted this point of view, progress on negotiations improved. Hence, their focus shifted to mitigating the damage from tariffs rather than attempting to avoid them altogether. As such, the situation remains fluid. Most tariff-related announcements were of preliminary agreements and not final. In addition, the administration continues to announce new tariffs, such as with steel and copper, which can make getting to a final agreement more chaotic. Nevertheless, it is encouraging to see progress because markets favor certainty even if the consequences are somewhat negative.

The U.S. International Trade Commission issues a statistic of the approximate effective tariff rate, which as of the end of July was 9.75%. That rate is up from 2.31% reported for November 2024. There are estimates from other sources that estimate a higher effective rate in the upper teens. Regardless of which figure is correct, it is the amount of increase in the effective rate that concerns investors. Interestingly, one of the biggest surprises to the markets this year is that the negative effect from those higher rates has not yet impacted the global economy to the degree expected earlier. For example, in September, the Organization for Economic Co-operation and Development increased its global GDP forecast for 2025, stating that the full effects of higher tariffs have yet to be felt. They stated that tariffs are rolling out more gradually than expected, and that firms are choosing to give up some margin by absorbing the tariffs rather than passing them onto consumers. Their outlook for 2026 did not change, up 2.9%, but they now assume the growth rate will decelerate year-over-year.

It will be interesting to see if this year’s momentum continues into the fourth quarter. There are still a number of very important deals yet to be determined — agreements with China, Mexico and Canada come to mind. Clarity on these three is paramount given they are the U.S.’s largest trading partners.

Download the PDF to continue reading this quarter's commentary.

CLICK HERE

Davidson Investment Advisors, Inc. is a SEC registered investment advisor. The opinions expressed herein are those of Davidson Investment Advisors and are subject to change.

The information contained in this presentation has been taken from trade and statistical services and other sources, which we believe to be reliable. We do not guarantee that this information is accurate or complete and it should not be relied upon as such.

This presentation is for informational and illustrative purposes only, and is not intended to meet the objectives or requirements of any specific individual or account. Past performance is not an indicator of future results. Indices provide a general source of information on how various market segments and types of investments have performed in the past. An investor should assess his/her own investment needs based on his/her own financial circumstances and investment objectives.

The information on indices is presented for illustrative purposes only and is not intended to imply the potential performance of any fund or investment. Index performance assumes the reinvestment of all distributions, but does not assume any transaction costs, taxes, management fees, or other expenses. Indices are not available for direct investment.

The S&P 500® Index is a gauge of large-cap U.S. equities and serves as the foundation for a wide range of investment products. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

The Bloomberg Intermediate U.S. Government/Credit Bond Index is a broad-based flagship benchmark that measures the non-securitized component of the U.S. Aggregate Index with less than 10 years to maturity. The index includes investment grade, U.S. dollar-denominated, fixed-rate treasuries, government-related and corporate securities.

The MSCI EAFE® Index is broadly recognized as the pre-eminent benchmark for U.S. investors to measure international equity performance. It comprises the MSCI country indexes capturing large and mid-cap equities across developed markets in Europe, Australasia and the Far East, excluding the U.S. and Canada. Numerous exchange-traded funds are based on the MSCI EAFE® Index, and the Chicago Mercantile Exchange, NYSE Liffe U.S. and the Bclear platform of Liffe are licensed to list futures contracts on this index as well.

The MSCI Emerging Markets® Index is a free-float weighted equity index that captures large and mid-cap representation across Emerging Market countries. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

The Bloomberg Dollar Spot Index tracks the performance of a basket of 10 leading global currencies versus the U.S. Dollar. It has a dynamically updated composition and represents a diverse set of currencies that are important from trade and liquidity perspectives.