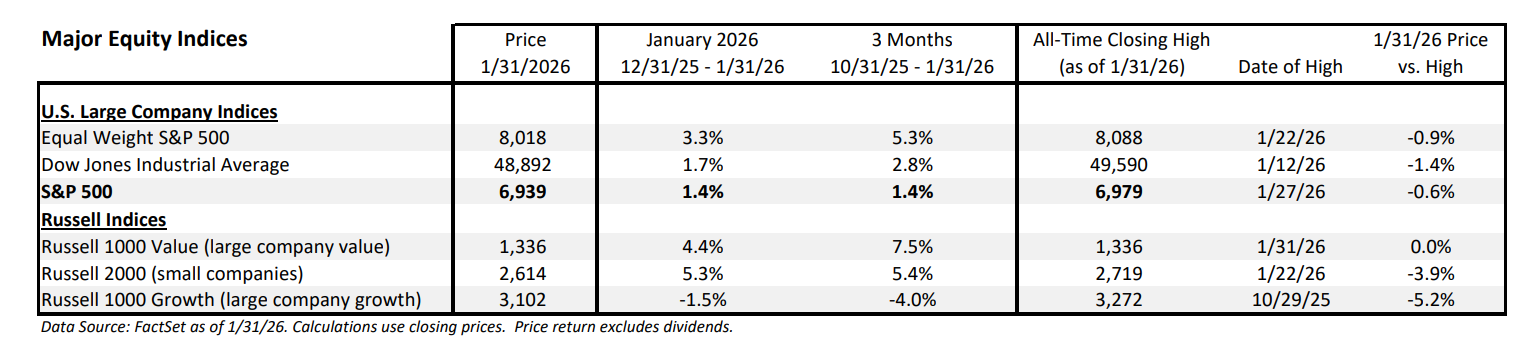

U.S. equity indices largely moved higher in January, and the widely followed S&P 500 equity index set a new all-time closing high price as recently as 1/27/26. But other indices set new highs as well, and the larger story of January, in our view, was a continuation of a rotation of leadership away from large-company growth stocks and into large-company value stocks and small capitalization stocks. The shift in sector sentiment began at the end of October, and over the three-month period that includes November, December, and January, the rotation became increasingly pronounced. From 10/31/25 to 1/31/26, the S&P 500 delivered a respectable +1.4% price gain, but the Russell 1000 Value Index increased +7.5% to lead U.S. equity market gains. By contrast, the Russell 1000 Growth Index decreased -4.0% over the three-month period. The Russell 1000 Growth Index has outperformed its value counterpart for 8 of the past 10 years, including each of the past three years. The last time, on an annual basis, that value stocks outperformed was 2022. The rotation of index leadership to value from growth was driven by sector rotation as we have seen a large divergence in sector performance in recent months. The three largest sector weightings in the Russell 1000 Growth Index (as of 12/31/25) were Technology, Consumer Discretionary, and Communications Services, while the largest three sector weights in the Russell 1000 Value Index were Financials, Industrials, and Health Care (it should be noted that Technology is the #4 weighted value sector, so value includes Technology, just in a much lower weight). The top three S&P 500 sector weights (as of 12/31/25) were Technology, Financials, and Communication Services. The S&P 500 screens as a growth index but does offer some value balance as Financials have the second largest weighting.

Will value continue to outperform growth?

We have argued for sector rotation for some time as a portfolio well-diversified across sectors can provide some protection from a pull-back in growth stocks, and because we see upside to economic growth estimates in 2026. Sustained economic growth can boost earnings results across cyclical industries, leading to broader participation in market gains. However, given recent underperformance of many leading growth companies despite relatively strong earnings results, we see the potential for a recovery. But, on market strength and throughout the year, we are comfortable adding exposure to value and reducing exposure to growth.

Continue reading our Market Strategy commentary.

CLICK HERE

Important Disclosure: Information contained herein has been obtained by sources we consider reliable but is not guaranteed and we are not soliciting any action based upon it. Any opinions expressed are based on our interpretation of the data available to us at the time of the original publication of the report. These opinions are subject to change at any time without notice. Investors must bear in mind that inherent in investments are the risks of fluctuating prices and the uncertainties of dividends, rates of return, and yield. Investors should also remember that past performance is not necessarily an indicator of future performance and D.A. Davidson & Co makes no guarantee, expressed or implied to future performance. Investors should consult their Financial and/or Tax Advisor before implementing any investment plan.

Market Indices: The information on indices is presented for illustrative purposes only and is not intended to imply the potential performance of any fund or investment. Indices provide a general source of information on how various market segments and types of investments have performed in the past. Index performance assumes the reinvestment of all distributions, but does not assume any transaction costs, taxes, management fees, or other expenses. You may not invest directly in an index. Past performance is not an indicator of future results. The S&P 500 Index is a market cap weighted index that is designed to measure the US large-cap equity performance. The index is composed of the 500 leading publicly traded US companies based on size, liquidity, industry, and profitability criteria. The Dow Jones Industrial Average is a price weighted index that tracks 30 large, publicly owned companies trading on the New York Stock Exchange (NYSE) and the NASDAQ. The Russell 2000® Index is a market cap weighted index that measures the performance of the 2,000 smallest companies in the Russell 3000® Index. The Russell 1000 Growth index includes the Russell 1000 companies that exhibit relatively higher price-to-book ratios, and higher expected earnings and sales growth. The Russell 1000 Value index includes the Russell 1000 companies that exhibit relatively lower price-to-book ratios and lower than average expected earnings and sales growth. The S&P 500 Equal Weight Index is the equal-weight version of the S&P 500, which is weighted by market capitalization. In the Equal Weight version, each company is assigned an equal weight, about 0.2%, and is rebalanced quarterly.